Feature Spotlight: Savings

Savings |

BudgetForLife's primary tool for the money that's left over

|

Why use Savings |

How to use Savings |

|

So you've gotten the hang of budgeting, keeping tack of your expenses and living within your means. Maybe you even have a little money piling up in your bank account. Now what? Use BFL's Savings tool, that's what!

Savings allows you to allocate money towards multiple goals simultaneously. That way, instead of just 'money in the bank,' you can have money clearly differentiated between your emergency fund, your house down payment fund, your vacation fund, and your car repairs fund - all within the same bank account! Savings also allows you to maintain balances for different types of accounts you may have. For example, your brokerage, your checking, and your HSA could each be their own savings goals, updated to reflect deposits, withdrawals, and gains or losses. Finally, Savings enables you to look forward. While Projections is where you want to be to plan ahead for incomes and expenses, Savings is where we do so for what's left over. |

Not every user implements their Savings tool in the same way. One of the best things about budgeting, after all, is that there's no 'right way' to do it, and BudgetForLife aims to maintain the customization needed to reflect that.

One thing that is unique about the Savings tool is that it's use changes as time passes within the life of your budget. Looking forward, Savings functions similarly to Projections. Users create any number of savings categories (goals), and decide on an amount to aim for each month within each goal. However, once that month transpires, we will want an accurate representation of what really happened with our savings - like the Timeline does for our income and expenses. Not only that, but we may want to keep a record of the difference between our expectations and reality - like the Accounts feature does for our expenses. These functions, too, take place within the Savings tool. Below we highlight the core functionalities of the Savings feature - future planning, real-time adjustments, and a historical record of goals and progress. |

|

Future Planning

|

The way we effectively plan for the future is by setting realistic yet challenging savings goals that motivate us.

|

|

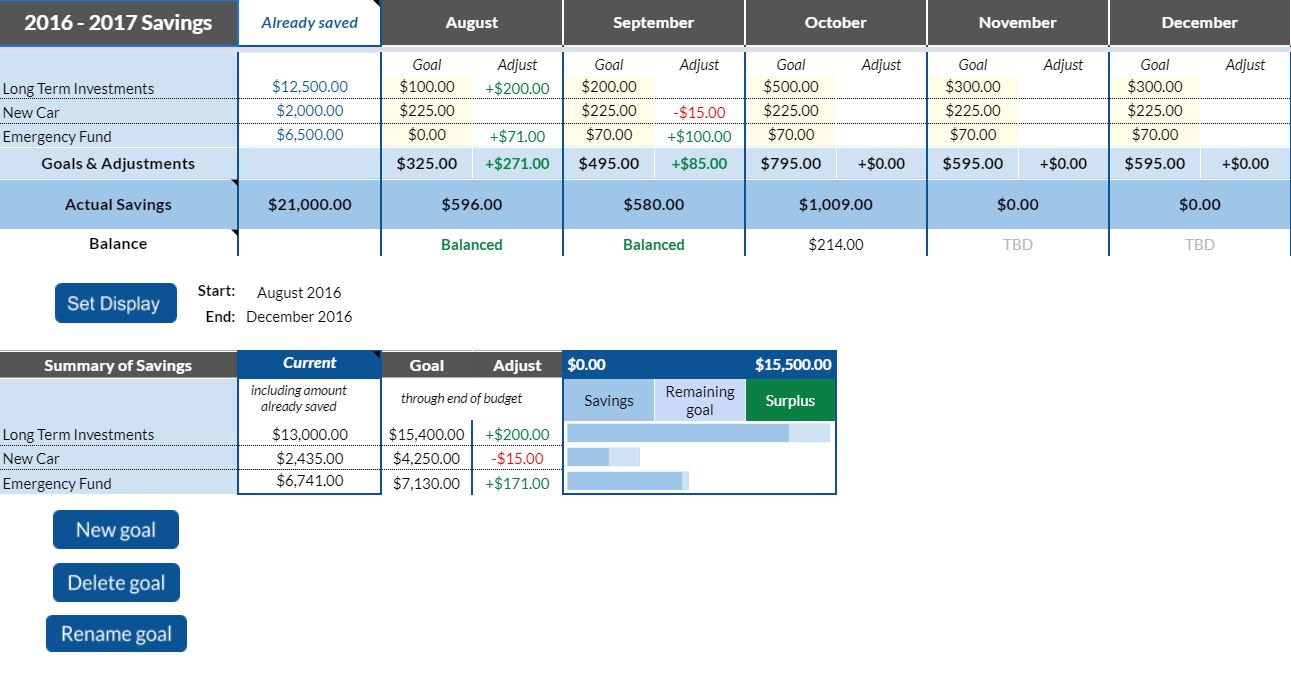

Step 1. Create savings goals

Use the buttons at the bottom of the sheet, to add, delete, and rename savings goals as you see fit. See the Savings FAQ at the bottom of this page for some ideas.

|

Step 2. Account for past savings

Based on your current bank account balances, consider how to best allocate these funds between your savings goals. Set these allocations manually in column B and adjust if needed.

|

Step 3. Set monthly savings targets for each goal

Decide how much you want to save toward your goals each month by entering the amounts into the cells colored sticky-note yellow under 'Target.' To get an idea of how much total your goals should add up to, evaluate Projections and/or Timeline.

|

|

Real-Time Adjustments

|

To get the most out of our savings targets, we change them as needed to reflect current circumstances

|

|

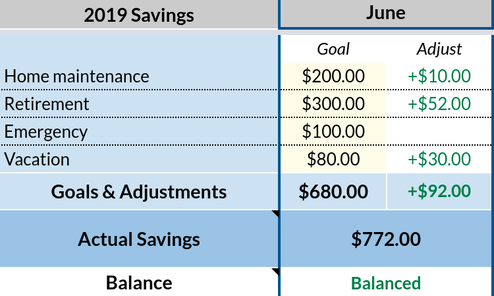

Example 1. Spending money from savings

If you're saving for a particular purchase, there will come a time to make that purchase. Or if you have a tough month, you may need to withdraw money from your investments. As it relates to any expenses, users should record them in the Log as usual. However, as it relates to our savings tool, it's important to ensure that our goals remain accurate. To illustrate these changes in expectations, adjust the Target of the savings goal(s) affected within the month of the purchase(s).

In this illustration, you save $200 per month in order to plan for unexpected home maintenance. In March, you have to spend $300 to repair an appliance. As a result, you change your goal for that month from $200 to -$100. This accounts for the $200 you routinely try to save minus the $300 you now expect to spend.

|

Example 2. Adding money to savings

Every now and then, you may have a fortunate and unexpected financial event occur that changes what you now aim to save for the month. Perhaps you receive a bonus from work or a generous gift from your wedding or graduation. The question is: does this income impact your savings targets? If not, and you plan on spending it all, then perhaps no action is necessary as it relates to your Savings tool. But, if you intend to save some, decide how much and to what goals you wish to put it towards. As in Example 1., to record these changes, update the Target(s) of the corresponding savings goal(s). In both examples, we edit the Target itself (rather than using the 'Adjust' column) because these real-time scenarios caused immediate changes of plan. When our intentions to save change, we update our Target, which tell us what we're aiming for in future months, in the current month, and what we aimed for in past months. And as we've seen, a wide array of circumstances may warrant an updated target. The Adjust column we'll discuss below.

|

|

Historical Records

|

Evaluating past months empowers us to stay disciplined with our spending and stay on track with our goals

|

|

Step 1. Balance your savings

Most months you are not going to save exactly the amount you expected. At the end of each month, you may want to take note of any surplus or deficit you have and give every dollar a clear purpose. This is where the 'Adjust' column comes into play. Adjustments illustrate the difference between our Targets and reality; they essentially reflect our ability to exercise restraint in our spending as well as the feasibility of our Targets themselves. If you exceed your expected savings for the month, designate which categories you'd like to contribute that surplus towards by entering the amounts directly in the corresponding 'Adjust' cells. And on the contrary, if you fall short, decide which savings funds that money should be pulled from. It's also possible to have a mix of both in the same month, where some targets you elect to adjust with additional funds whereas others you adjust by deduction. The key to note that once every dollar is accounted for, the bottom cell reads 'Balanced.' |

|

|

Step 2. Tracking with your savings goals

With your savings figures balanced via your Adjustments, you have now given each of your saved dollars a purpose toward one of your goals. At the same time, you have a record of whether you exceeded or fell short of your original goals. At the end of each month, figures at the bottom of the Savings tool automatically update to reflect your current progress towards your targets. If you're behind schedule, consider how you may be able to cut back spending or earn extra money in the months you have left in order to catch up. If you're ahead of schedule, way to go! It's a great feeling, isn't it? :) |

|

Savings FAQ

What Savings goals should I have?

The short answer is, whatever you find helpful! Remember that your budget exists for your benefit, and as such, the types of goals you choose are completely up to you. That said, here are some example objectives that some of our users implement:

The short answer is, whatever you find helpful! Remember that your budget exists for your benefit, and as such, the types of goals you choose are completely up to you. That said, here are some example objectives that some of our users implement:

- Saving for a large item/purchase over the course of many months. This could be for a laptop, vacation, engagement ring, car, phone, home, piece of furniture, or otherwise.

- Preparing for inconsistent expenditures - costs that are bound to happen eventually, but you can't predict when they will occur. Things like auto maintenance, house maintenance, or medical needs. You may want to put away a certain amount each month in order to be prepared for when those expenses arise.

- Investing for the long-term. Some of our savings (such as for retirement, future college tuition, or an emergency fund) might not have a hard date attached; however, allocating money towards these goals is often prudent.